On-Demand Transit 2024 Market Report

Good news first: What initially appeared to be a weaker year at the midyear point, 2024 has managed to come out on top, setting a new record with close to 400 new projects launched in the past 12 months. But upon zooming in, 2024 reveals interesting dynamics with potentially less positive future consequences for the market.

On-Demand Transit World Map (all projects)

On-Demand Transit World Map (currently active projects only)New Record Year, New Drivers of Growth

2024 saw change in geographical dynamics: Some markets got kicked into overdrive while hitherto growth drivers plunged. In total, over 390 new projects were launched which is a new record, despite the first two quarters of 2024 starting slower than in the year before. What appeared to be first signs of cooling growth, 2024 impressively rebounded in the second half of the year — and Q4 was just plain crazy.

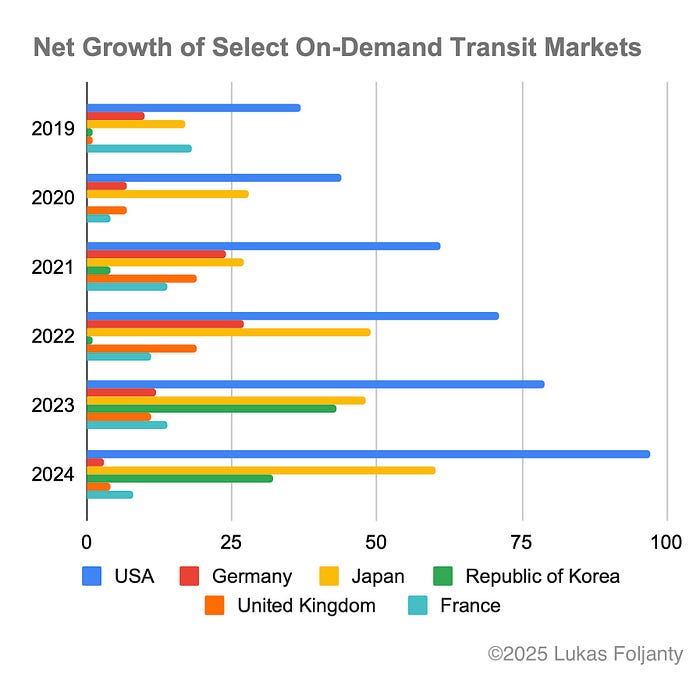

The exceptional growth in Q4 came from East Asia with South Korea continuing its impressive development of recent years, totalling at close to 50 new projects in 2024. But Japan took it to another level altogether: Over 50 launches in Q4 alone! Besides the “usual suspects” Koga Software with its Choisoko services and ever-busy Mirai Share, Spare-powered Know Route made a huge leap in 2024 with close to 20 new services. In total, Japan saw 100 new projects come to market and the net market growth (new projects launches minus projects ending) was an impressive +60.

The USA remained on a steady course in 2024 with approximately 120 new projects launching and a net growth of around +100.

Things look less positive in Europe, though. What used to be one of the main growth regions of On-Demand Transit took a heavy hit in 2024. While the total number of new services still stands at around 100, the net growth halved in comparison to 2023 to just +30. Particularly crass is the slump in Germany, one of the forerunners and former driver of global market growth. Germany barely achieved a positive net growth with only +3 more projects launching than ending. Main reason for this negative trend is the discontinuation of European, federal and state grants which necessitated municipalities to critically evaluate their pilot programs with many deciding to not transition their pilots into revenue services. A particularly notable victim is Berlin’s on-demand bus service ‘Muva,’ which is the successor to the once-largest on-demand ridepooling service, ‘BerlKönig.’ Muva’s open-to-all Ridepooling service is scheduled to end prematurely in February 2025, with only the paratransit-esk contingency bus service for broken subway elevators continuing until the full contract term. Given that the current state government of Berlin is considered car-friendly and facing the need for budgetary cuts, one must wonder if the elevator contingency service will be extended beyond the contract term at the end of 2025.

Which raises an interesting question: Is Germany simply ahead of the curve, and will other markets with a high degree of third-party funding experience similar effects, albeit with a time delay? Especially the United States seems at risk of facing a similar fate in a few years, considering the massive federal funding pumped into the system under the Biden-Harris administration, which also strongly benefited the microtransit boom of recent years. While ex-FOX business host and new US DOT Secretary Sean Duffy didn’t give many clues on his agenda for transit in his Senate confirmation hearing, one must wonder whether the new administration will be as committed as the previous one to investing in making transit more attractive to a wider audience — especially if the the President’s new darling adviser is a known hater of public transit who’s solution to traffic congestion is to build a tunnel for taxi-like individual transport. Possibly in an act of calculated optimism, multiple US On-Demand transit solution providers emphasised the bipartisan support for public transit (e.g. here, here or here). APTA seems worried, though, which feels like the right instinct, considering that Project 2025 seems to strongly favour individual transport and calls for reductions in federal funding for transit — which might bring aforementioned new Head of the Department of Government Efficiency back into the picture? I guess time will tell…

Meanwhile in Dubai, three new pooled on-demand commuter services launched in late 2024 by Kuwait’s CityGroup on its door2door platform (CityLink Shuttle), UK-based WeMove, which deployed its own tech for the first time (DrivenBus), and local transport operator company GateZone with Liftango (Fluxx Daily). These are B2C services, but in a tight corset of rules and regulations (areas, pricing, etc.) by Dubai’s omni-powerful Road Transport Authority, which awarded the concessions through a RFP procedure. The same RTA also provides a public On-Demand Bus service, operated by UnitedTrans on Via’s tech. It will be interesting to observe how these services will perform and whether this is going to be a viable business for the providers.

And speaking of the MENA region, Voyagerr won a large tech contract for the on-demand bus in Riyadh, Saudi Arabia, despite Via’s multi-year partnership with the Saudi Public Transport Company (SAPTCO). Which could be taken as a sign that the “old” tech providers are by no means out of the game.

By the end of 2024, over 2,000 On-Demand Transit services have been launched globally since 2012 with over 1,300 currently active.

The Gloves Are Off — Tech Provider Market Update

The On-Demand Transit space has been a fiercely competitive battleground for years, also during periods when public transportation budgets were bolstered by third-party funding. And that didn’t change in 2024, perhaps best exemplified by Spare giving away their technology for free for a 3-year contract with LA Metro, which LA Metro’s board celebrated as a reduction in software costs of $928,521 for the first year in comparison to the previous contract with RideCo. Via was awarded the separate operations tender with a volume of around $45M for the same contract term. I guess either the tech providers are now so well off that they can afford to waive close to a million dollars in annual recurring revenue, or the race to the bottom in SaaS fees has really hit rock bottom now.

And while we are at tech providers at each other’s throats: Via won its patent infringement lawsuit against RideCo. The jury found that RideCo infringed three of Via’s US patents concerning the concept of dynamic routing between virtual stops depending on walking distance to/from the stop, vehicle location, demand prediction, traffic intensity, and other criteria. Via has undoubtedly invested significant resources into developing a sophisticated routing and ride-matching algorithm and it’s understandable that they are trying to protect their intellectual property. But it makes one wonder about the fallout of this verdict. Essentially, all On-Demand Ridepooling technologies are based on this concept — and arguably, Via wasn’t the only one to come up with it (Kutsuplus anyone?). But apparently they were the only (or first?) ones to patent it. So now RideCo was ordered to pay $US1.4M in damages to Via, which it intends to appeal. But what happens if the verdict stands? Is Via going to go after the other (US) tech providers, too? And how will tech providers battling it out in court affect the notoriously risk-averse public transit industry’s trust in the concept and involved players?

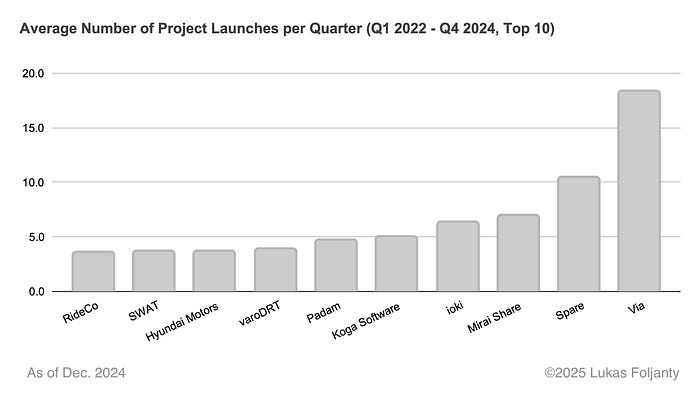

The ranking of tech providers by the number of projects looks very similar to previous editions of this report. Via has surpassed the 400 projects mark and Spare has surpassed 200. The two South Korean players Hyundai and varoDRT are now well-established in the Top 10 of this ranking.

As a bit of a sneak-peak into 2025, it’s worth mentioning that Blaise is expected to break into the Top 10 with a wave of launches in January 2025 on the back of its large multi-service contract in Nova Scotia, Canada. And as another sneak-peak, there’s yet another company coming to market in 2025 and trying their luck: Publicly traded Argo, founded by ex-Uber managers, promises to make “public transit […] faster than driving a car but as affordable as taking the bus.” They plan to launch their first public service in Bradford West Gwillimbury, Canada in Spring 2025. I guess we’ll find out whether they are going to crack the nut of PRT by being “[…] able to deliver viable and scalable economics that are competitive with existing systems by driving more people into transit and deploying the vehicles only as they’re needed.” (source)

Overall, Via has around 24% market share on global level with its most significant markets being North America, DACH and Europe, but its most dominant markets being the much smaller markets MENA and Australia/New Zealand. In Asia, on the other hand, Via seems to be struggling against local players or more potent in-market partnerships, such as Spare-powered Next Mobility by Nishitetsu and Mitsubishi in Japan, which successfully leverages both companies’ reputation to actively build a serious business in the public on-demand bus space.

Aforementioned partnership also helped Spare in the average number of service launches per quarter where it surpassed the 10 services mark in the Q1 2022 to Q4 2024 timeframe. Via remains in a league of its own with over 18 service launches on average per quarter, thus widening the gap to the competition with every quarter. As I predicted in my last report, both South Korean players are now among the top ten in this benchmark.

Meanwhile, SWVL seems to have abandoned its B2C business and is now solely focussing on B2B and B2G contracts, such as the recently announced first/last mile employee transport service for SAB Bank in Riyadh, KSA. Doubters remain sceptical about SWVL’s future outlook, though.

On the funding front, the biggest news came from Spare which raised $42M in Series B in September 2024, of which they invested a healthy dose into winning (or what do you call this?) the LA Metro tech contract. Earlier in 2024, SWAT Mobility ($7.2M) and Freebee ($5M) also raised. But still no word of Via’s IPO…

Welcome to the Niche — Project Characteristics

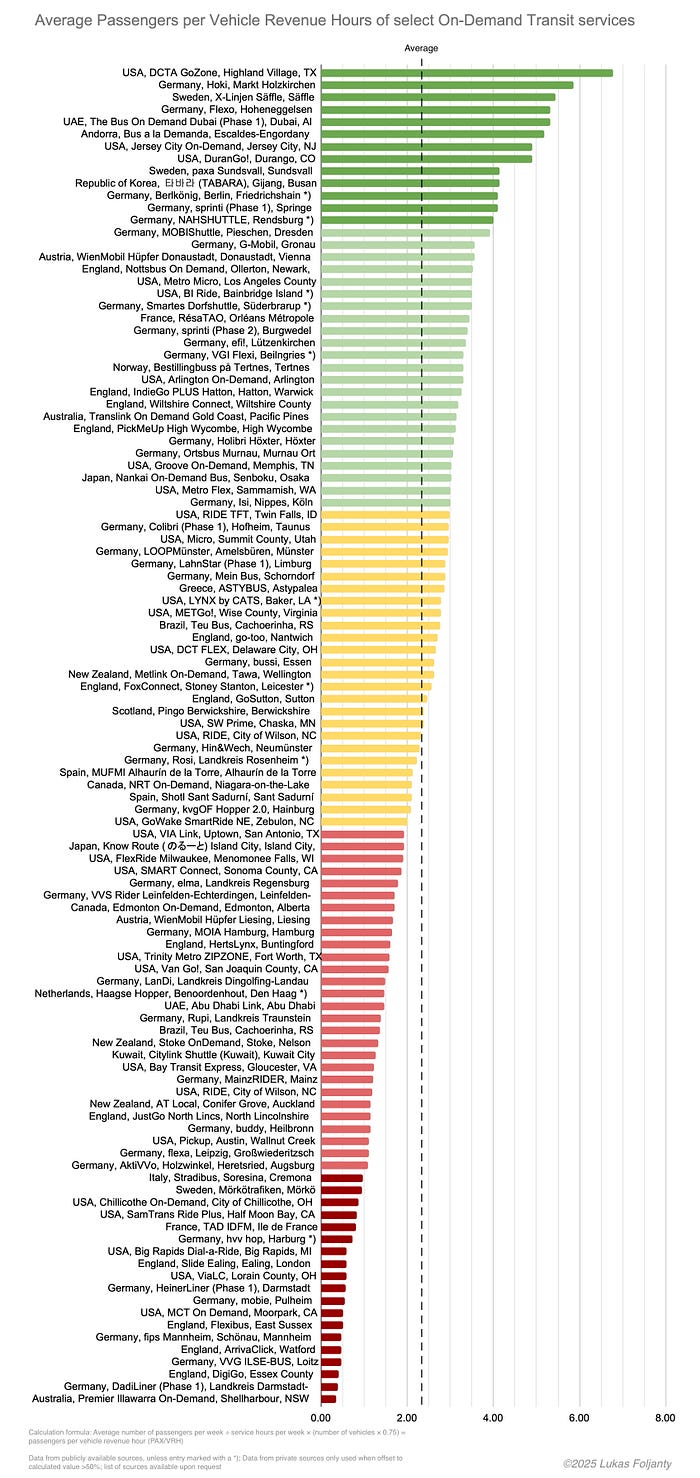

Public transit remains the main use case for pooled on-demand mobility. While the public sector has played a dominant role in the stellar growth of the On-Demand Transit market for years, 2024 saw a further increase in its share: 86% of the new services launched in 2024 were initiated and funded by the public sector. As discussed earlier in this article, there is an inherent risk in the heavy reliance on public funding, which is elevated if the services fail to deliver the expected performance. How the targets are defined differs from service to service. But a prevalent pitch of On-Demand Transit is its efficiency. One way to measure efficiency is the average number of passengers per vehicle revenue hour (PAX/VRH). Analysing the performance with the help of publicly available data (background on methodology) reveals a mixed picture at best.

111 examined services from 22 countries provide following indication to the efficiency performance of On-Demand Transit services:

- The average PAX/VRH is 2.34.

- 13 services performed very strongly with over 4 PAX/VRH and are probably maxing out what can be achieved in demand-responsive transport. As previously pointed out, there is no recognisable pattern to these services (use-case, location, demographics, price, etc.), which suggests that it has mostly to do with the service design and less so with the technology deployed.

- With 3–4 PAX/VRH another 23 services delivered solid results.

- However, 68% of my sample achieved less than 3 PAX/VRH, which I would define as minimum threshold to justify the efficiency pitch of On-Demand transit. More concerningly, 49 services achieved fewer than 2 PAX/VRH, raising serious doubts about whether these services are suitable for real-time optimised pooled on-demand transportation.

As pointed out before, not all services exist because of efficiency goals and thus, some PTAs might be totally fine with their On-Demand bus achieving low PAX/VRH numbers. It still raises the question, though, if a different mode of operation might be the better choice in these cases. And it’s also worth pointing out that high efficiency results don’t necessarily mean that these services also perform well commercially.

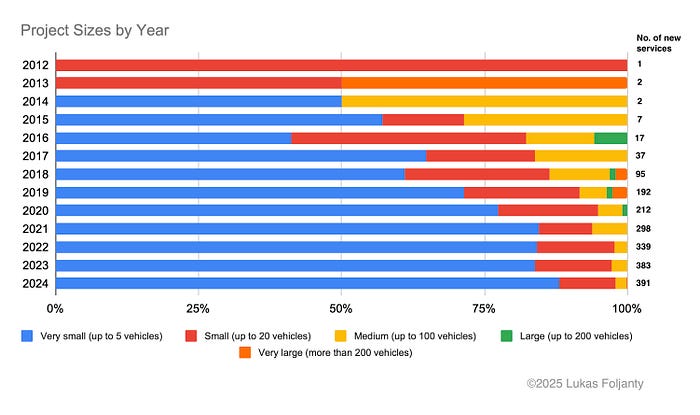

In terms of fleet sizes, the trend from previous years continued into 2024, with On-Demand Transit projects remaining very small. Ninety-eight percent of the newly launched projects had fewer than 20 vehicles, and 88% even featured five or less vehicles. The average fleet size for all newly introduced On-Demand Transit services in 2024 was six vehicles. This correlates strongly with the type of use-cases that dominate. Around 30% of all On-Demand transportation services in 2024 were introduced in rural settings, which due to their low population density usually only justify very small fleets (four vehicles in average in this segment).

Fleet sizes are much larger in the paratransit segment, which is the new battleground for the solution providers. Consequentially, the largest launch in 2024 was London’s 300 vehicles strong paratransit Dial-a-Ride service, which Via was contracted with.

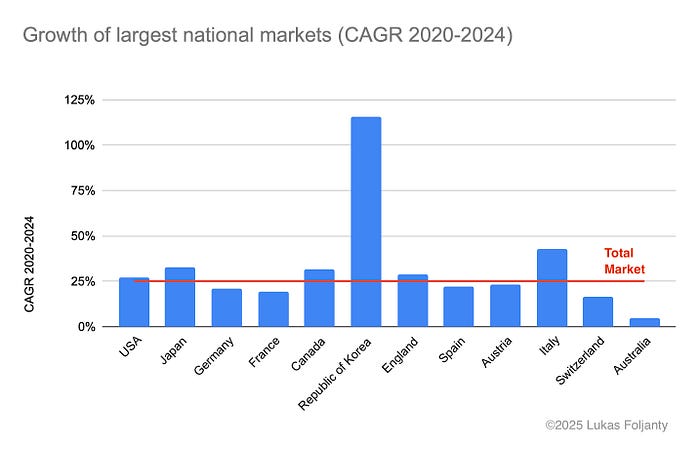

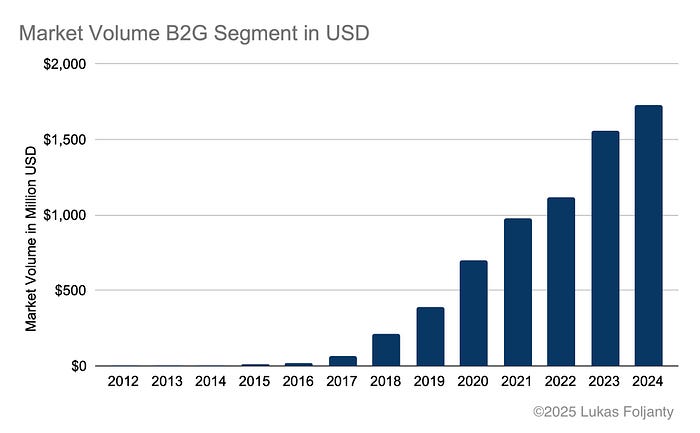

The fleet size is also a relevant KPI to determine the market volume from a monetary perspective. Due to the lack of available data, I borrow from a methodology called Reference-class Forecasting, which allows me to estimate the market volume from only three datapoints (details on methodology): Fleet size, project duration (months) and total project budget (technology, vehicles, drivers, operations etc.). By calculating the average budget per vehicle per year — which is approximately $225,000 in the On-Demand Public Transit (B2G) segment — I can determine the total market volume based on the number of active services and the average fleet size each year: The total market volume in the B2G segment in 2024 was around US$1.7Bn, which translates into a Y-o-Y growth of around 11% and a CAGR 2020–2024 of 19,8%. It’s important to note that this value includes all aspects of the value chain, with operations naturally accounting for the largest share in absolute terms, though contractors typically experience a lower margin. However, when top-line growth is crucial for the investor narrative, operations can still be a worthwhile business to pursue — as Via demonstrates — despite the limited scalability and the potential for dissatisfaction among PTOs, who could otherwise be customers on the technology side. Conversely, technology accounts for only about 15% of the total value but typically has higher margins — at least in theory, unless the market is engaged in a race to the bottom of SaaS fees.

Conclusions

2024 was the new record year with close 400 new services launched. From a total market perspective, the trend of previous years was prolonged and the growth trajectory continued to point upwards. However, 2024 was also the year in which a major concern of the market’s dependency on third-party funding materialised.

Germany, as one of the front-running markets, which used to grow consistently over the last years, took a heavy hit with a negative Y-o-Y growth in the number of new launches and barely a net positive growth in the number of active projects. Other European markets such as England or Austria were not much better off. Which raises the question whether this is a Europa-specific phenomenon or a foreshadow for what’s to come in other matured markets as well?

Much depends on what happens under the new administration in the U.S. Will strengthening public transit remain a policy goal, and will funding continue to be provided at the federal level?

Or is it perhaps time to direct the attention to other regions of the world, such as MENA or Asia? But are the currently dominating incumbents from Western countries well positioned to win these market regions? Or are we going to witness the rise of new market leaders on the back of strong home markets — and what is their expansion strategy going to be like? 2025 might give us an indication of what to expect.

About this Report

Hi, my name is Lukas and I have been writing this series of reports on the state and outlook of the On-Demand Transit market since 2020. I would like to provide some background and context so that you know how to read this article:

- Between 2017 and 2024, I was working at a range of On-Demand Ridepooling solution providers (check out my LinkedIn profile if you are interested in which ones). I started this series of articles in response to the lack of data on this new market. It has always been a private project and was never part of my work at any of the On-Demand tech providers.

- The market is not so new anymore, but it prides me that my dataset, which is the basis for my reports, is still the most comprehensive source. This is to no small parts thanks to the On-Demand Transit community which has been extremely supportive by providing data and feedback.

- Nevertheless, all findings shared in the article should always be understood as informed indications, not hard facts. I invest many (many) hours before writing each edition of this report for updating my extensive dataset and try to be as diligent as I can. But there will be gaps and errors. If you notice either, please drop me a note!

- I try my very best to keep this report vendor-neutral. That will not stop me from expressing opinions about the state of the market or market participants (sometimes possibly provocative). However, should you ever have the impression that I am not being fair in how I present my findings, I appreciate if you send me a message and let me know.

- Possible deviations of facts and figures to previous articles of mine are most likely caused by retroactive additions to the dataset, which have been made possible in part by feedback and support from the On-Demand Ridepooling community. I appreciate the overwhelmingly positive and open response to my articles!

- The Google world map gets updated in the background, so it might show services which are not yet reflected in the analysis of this article.

- I use following terms synonymously: On-Demand Ridepooling, On-Demand Transit, On-Demand Transport, Microtransit, DDRT.

- The views expressed in this article are my own. They do not purport to reflect the opinions or views of my current employer.